Am I being too bullish on China or am I reading all the data wrong? But guess what ,China's growth needs re-orienting viewed in terms of its current dependence on investment, currency controls, loose money etc...Though capacity utilization is at 100%..it makes me worried as in conjunction with what is happening in EU and the current mayhem in markets in the US,

It is best China taps some of its domestic constituency and unleash it...It has so many strengths in terms of consumption spending power and domestic demand in general...

It is best China taps some of its domestic constituency and unleash it...It has so many strengths in terms of consumption spending power and domestic demand in general...

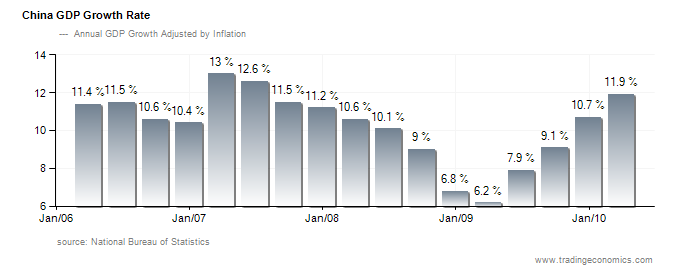

A sizzling 11.3% growth in Q1 and a consistent 8% plus avg. growth that has been envious...While the Chinese will do anything to keep unemployment down....

Recipe for Inflation: China mostly is in the grip of a bubble as its property markets are indicating and are so are credit markets. People's Bank of China recently revealed that in March the output gap reached more than 3%, the highest level since 1998 and the seventh straight month of increase. Positive output gap indicates that factories are running out to comply with high demand which in turn is likely to push prices even higher. This looks very inflationary for China in conjunction with the very level of money supply.

People's Bank allowed lending to surge starting in late 2008 to fight the global financial crisis. New loans rose to a record 9.59 trillion yuan in 2009 and banks advanced another 3.38 trillion yuan in the first four months this year. The Shanghai Composite index of stocks has fallen off more than 2o% this year, the worst-performing index in Asia, as investors sold Chinese assets on concern a withdrawal of stimulus spending and a slowdown in construction could choke off growth after an 11.9% expansion in the first quarter. (Thanks CNBC)

In Shanghai fears abound that property speculators chasing quick profits are inflating a real estate bubble. Apparently, the Chinese Government is also worried about this and is now capping prices and making some building loans harder to get.

Re-orientation critical as current strategy has outlived utility

Besides PBoC's March 2010 data, that China is facing serious overcapacity problems goes beyond real estate. According to Prof. Michael Pettis lectures of Peking University, China's understandable efforts to try and shield itself from the world economic crisis with a massive stimulus package may end up making its situation worse. I am also getting a feeling that China has reached a point where it is producing stuff or investing in infrastructure that is not economically viable; that in the future China is still not going to be able to use this stuff and Chinese people are still going to have to pay for it despite the negative NPV of so many road projects.

Pettis conclusion is stark "when that happens that will exchange future growth in exchange for the growth that we got today." "What we've seen in the last year has been a very robust reaction to the contraction in the export sector and to the threat of rising unemployment." Professor Pettis says China entered the global financial crisis with an investment rate that was probably much too high.

Look at the Chart below and it is easy to understand why China needs to stimulate consumption. The economy is way too heavily dependent on investment. Since investment rates is so high there's a very, very strong reason to believe that a lot of this investment is being wasted. Considering the monetary policy in place to allow for easy access to capital, repayment nightmares could become a big potential issue that makes any growth very inefficient....

China is not imploding any time soon as doom mongers seem to suggest.....nothing the Chinese cannot handle...

No comments:

Post a Comment